How Much Does It Cost to Sell a Home in Lake Geneva, WI?

Quick answer: Most Lake Geneva sellers pay negotiated broker compensation, the Wisconsin real estate transfer fee of $3 per $1,000 of sale price, property-tax proration, their remaining mortgage payoff, and title or association charges. The total depends on your price, closing date, and the terms of the accepted offer. The most reliable figure comes from a seller net sheet built for your specific property, not a percentage rule of thumb.

Selling a Lake Geneva home creates a group of costs that come out of the sale proceeds. Some are predictable. Some move with the offer. And a few only show up on lake-access, condominium, or association properties.

Kim and Joel Reyenga prepare a net sheet before you list, so the expected proceeds are clear before an offer ever arrives.

Here is what typically comes out of a seller's proceeds at closing:

-

Broker compensation stated in the listing agreement

-

Wisconsin real estate transfer fee

-

Property-tax proration for the year of closing

-

Mortgage payoff, daily interest, and any lender release charges

-

Title, deed, recording, association, or closing charges assigned to the seller

-

Seller credits, repair agreements, or personal-property agreements from the offer

Each line changes with the price, the closing date, and the deal terms. That's why an estimate for your address beats any statewide average.

Start with a net sheet, not a percentage

A seller's net is the amount left after transaction costs are paid from the sale proceeds.

A net sheet estimates that number before closing. The title company then produces the final settlement statement once the offer terms, payoff figures, tax proration, and closing charges are known.

The basic framework looks like this:

-

Proposed sale price

-

minus broker compensation stated in the listing agreement

-

minus the Wisconsin real estate transfer fee

-

minus estimated property-tax proration

-

minus mortgage payoff, daily interest, and lender release charges

-

minus title, deed, recording, association, or closing charges assigned to the seller

-

minus seller credits, repair agreements, and personal-property agreements

-

equals your estimated seller proceeds

Kim and Joel prepare the first net sheet before the home goes live. It gives you a working estimate of what the sale could produce at several price points, which is a much better decision tool than a guess.

You can start with a and a look at , then ask us to build a net sheet around the likely list-price range.

Broker compensation is negotiated

Broker compensation is set by agreement. It isn't a state-set fee.

Your listing contract states the compensation terms for the work involved in the sale: pricing, preparation, marketing, showing coordination, offer review, transaction coordination, and communication from list to close. The final closing statement then reflects the amount due under the transaction documents.

Discuss the terms before you sign a listing agreement, along with the marketing plan, the showing process, communication expectations, and your goals for the sale. A clear conversation early prevents surprises later.

For the full listing process, read . To set the number itself, see , then when you're ready to see the figures for your property.

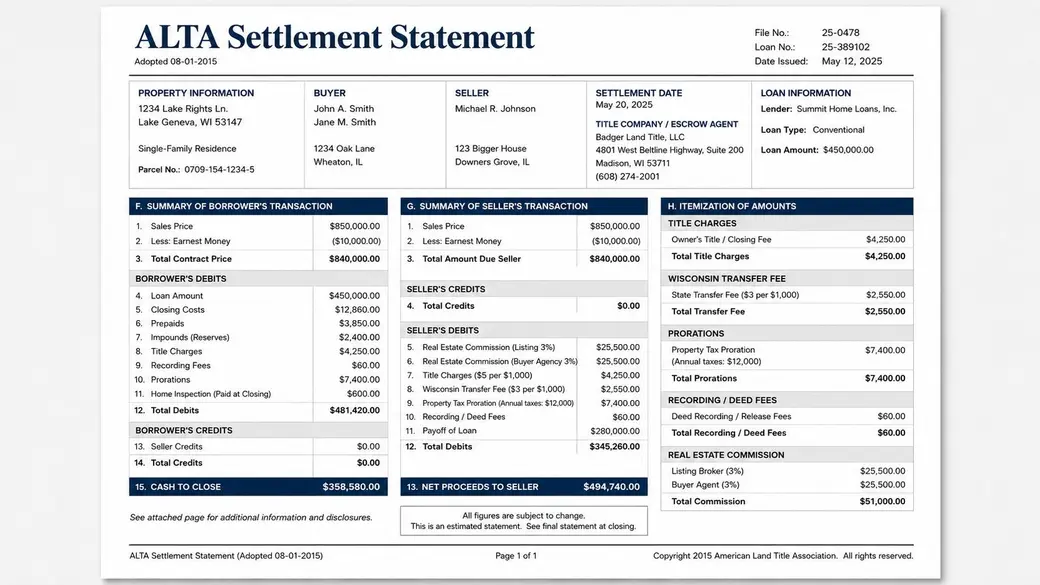

The Wisconsin real estate transfer fee

Wisconsin charges a real estate transfer fee on most taxable conveyances.

Under the Wisconsin Statue the fee is $3 for each $1,000 of value, or fraction of $1,000. The grantor (the seller) is responsible for the fee unless an exemption applies.

Here's how the math works on a $500,000 sale: divide $500,000 by 1,000 to get 500, then multiply by $3. The transfer fee is $1,500.

The explains the online filing and payment process. The Department also notes that some seller expenses paid by a buyer can be included in the value subject to the fee, which matters when an offer shifts certain seller costs to the buyer.

We add the estimated transfer fee to your net sheet before you list. For most traditional sales, it's one of the more predictable line items.

Property-tax proration is often the biggest variable

Property taxes can make a real difference in your proceeds, especially for Lake Geneva-area homes with higher assessments or special district charges.

The accepted offer states how taxes get prorated at closing. The Wisconsin WB-11 Residential Offer to Purchase includes several proration formulas: the prior year's net general real estate taxes, current assessment times current mill rate, and a formula tied to sale price and local assessment practice. The offer may also include a re-proration agreement once the actual tax bill arrives.

That flexibility matters because the tax bill for the year of closing may not be final when you sign. Reassessment, remodeling, new construction, credit changes, or a mill-rate change can all move the final number.

Kim and Joel review the current tax bill, any reassessment notices, and the offer's proration language before you accept. The offer controls the calculation used at closing.

Mortgage payoff and lender charges

If you still carry a mortgage, the closing agent requests a payoff statement from your lender.

The payoff usually includes the remaining balance, daily interest through the payoff date, and any lender release or administrative charges. Because the exact figure moves with the closing date, the first net sheet uses an estimate and the final settlement statement uses the lender's payoff demand.

The same early review applies to a home equity line, a solar loan, a private loan, a judgment lien, or any other recorded obligation. Bring those items up before the property goes live.

A payoff issue found after an accepted offer can delay closing or shrink your proceeds. We help sellers surface the questions early, then the title company and lender confirm the exact figures.

Seller credits and inspection agreements

A buyer may ask you to contribute toward closing costs, repairs, prepaid items, or other negotiated terms. You can agree, counter, or decline, and each choice changes your net.

Inspection negotiations affect proceeds too. You might make a repair, credit the buyer, reduce the price, or leave the offer as written. The right call depends on the issue, the request, your other options, the condition of the home, and the rest of the offer.

Kim and Joel review the entire offer, not just the sale price. A higher price with large credits, shaky financing, or a tight timeline can net less than a lower offer with cleaner terms. The net sheet shows you that difference in dollars.

If you're preparing for a busy selling season, walks through pricing and presentation that protect your bottom line.

Title, deed, and closing charges

Title and closing costs depend on the contract, the title company's fee schedule, recorded liens, deed preparation needs, local recording charges, and the services required to close.

You may see charges tied to title work, deed preparation, payoff processing, wire fees, courier fees, recording, lien releases, or escrow services. Some of these can be negotiated in the offer.

Ask for a preliminary estimate as soon as you have a likely sale price. The final statement should match the accepted offer and the title company's closing instructions. Review it before closing, especially when the home has an existing mortgage, association dues, rental income, personal property, or multiple owners.

Condos, associations, and lake-access properties need another pass

A Lake Geneva-area property can carry costs that aren't obvious from the listing.

Condominium and association sales may involve document fees, resale certificates, transfer charges, unpaid assessments, or approvals required by the association documents. You may also need to address outstanding special assessments, rental restrictions, or ownership rights tied to a shared pier, beach, marina, or access parcel.

Those details show up across our market, whether the property is lakefront, lake-access, a golf-community condo, or an in-town home. The exact responsibility depends on the offer, the association documents, and the closing instructions.

Kim and Joel request these records early. Buyers want accurate answers before they commit, and you need the same records to understand your likely closing costs. The helps buyers research properties in the area, and a well-prepared seller gives them the documents that answer the ownership questions behind the listing.

Costs you may spend before the sign goes up

Some costs never appear on the closing statement, but they still affect your bottom line.

You might pay for cleaning, painting, landscaping, storage, moving, a repair, personal-property removal, or minor updates before the listing launches. Owners of seasonal or second homes often plan around personal use, dock and boat storage, contractor timing, and possession dates as well.

We help sellers separate the work that strengthens your market position from the work that can wait.

If the home is used during the summer season, set your showing availability and move-out timing early. The is a simple way to track public activity around the lake as you choose showing windows and a possession target. You can also browse for the lifestyle side of lake, golf, town, and country living that buyers are shopping for.

Capital gains and income taxes are separate from closing costs

A sale can raise federal or state income-tax questions: capital gain, adjusted basis, depreciation recapture, inherited-property basis, or a possible exclusion for a qualifying principal residence.

Those questions sit outside the title company's closing-cost estimate.

A CPA or tax adviser should review your situation before you list, especially for a second home, a rental, an inherited home, or a residence you've owned for many years. Bring the likely sale price, estimated closing costs, purchase records, improvement receipts, and prior depreciation information to that meeting. Good tax planning starts before the accepted offer.

We're licensed real estate agents, not attorneys or tax advisers, so treat this as general information and confirm the specifics with the right professional.

Your net sheet should be updated more than once

Kim and Joel prepare the first net sheet before launch, then update it when an offer arrives.

We update it again after inspection negotiations, after any credit or amendment, and after the final lender payoff. That gives you a clear picture at every decision point.

The goal is simple: you should know what the sale is likely to produce before you accept a contract, and again before you sit down to close.

Frequently asked questions

How much does it cost to sell a home in Lake Geneva, Wisconsin?

The total depends on the negotiated broker compensation, the Wisconsin transfer fee, property-tax proration, your mortgage payoff, title or association charges, and any seller credits or repair agreements. A net sheet gives you a property-specific estimate before you list, which is more accurate than a flat percentage.

What is the Wisconsin real estate transfer fee?

Wisconsin's transfer fee is $3 for each $1,000 of value, or fraction of $1,000, on most taxable conveyances. On a $500,000 sale that's $1,500. State law assigns the fee to the seller unless an exemption applies.

Does the seller pay the buyer's closing costs in Wisconsin?

A seller may agree to a buyer credit or contribution as part of the offer negotiation. The amount and purpose should be written into the accepted offer and included in your net-sheet review, since a credit reduces your proceeds.

How are property taxes handled when selling a Lake Geneva home?

The accepted offer states the tax-proration formula. The closing statement uses that contract language to divide the property-tax responsibility between buyer and seller for the year of closing, and the offer may allow a re-proration once the actual bill arrives.

What mortgage costs come out of my sale proceeds?

The closing agent uses your lender's payoff statement, which generally includes the loan balance, daily interest through the payoff date, and any lender release or administrative charges. A home equity line or other recorded lien is paid the same way.

Are capital-gains taxes included in seller closing costs?

No. Capital-gains and income-tax questions are separate from the closing-cost estimate. A CPA or tax adviser can review your basis, improvements, ownership history, and possible tax treatment before you list.

Request a Lake Geneva seller net sheet

Thinking about selling in Lake Geneva, Williams Bay, Fontana, Geneva National, Delavan, Elkhorn, or anywhere in Walworth County?

Categories

- All Blogs (128)

- Fontana (9)

- Geneva National (3)

- Lake Geneva (29)

- Lake Geneva Area Homes (10)

- Lake Geneva Buyers Guide (5)

- Lake Geneva Real Estate Market Update (2)

- Lake Geneva Sellers Guides (5)

- Lauderdale Lakes (2)

- Walworth County Market Updates (3)

- Whats Happening at the Lake (30)

- Williams Bay (6)

Recent Posts